Retirement annuities built for long-term financial security.

Plan, save, preserve, and retire with confidence through tax-efficient retirement annuity solutions from Sanlam, Old Mutual, Momentum and Discovery — with professional advice from Lebon Consulting and digital access through our secure client portal.

A retirement plan built around your life, not a template.

A retirement annuity is one of the most important long-term savings vehicles in South Africa — but the right structure depends entirely on your circumstances. Lebon Consulting assesses your full position before recommending a contribution strategy and product fit across our panel of leading providers.

What we assess

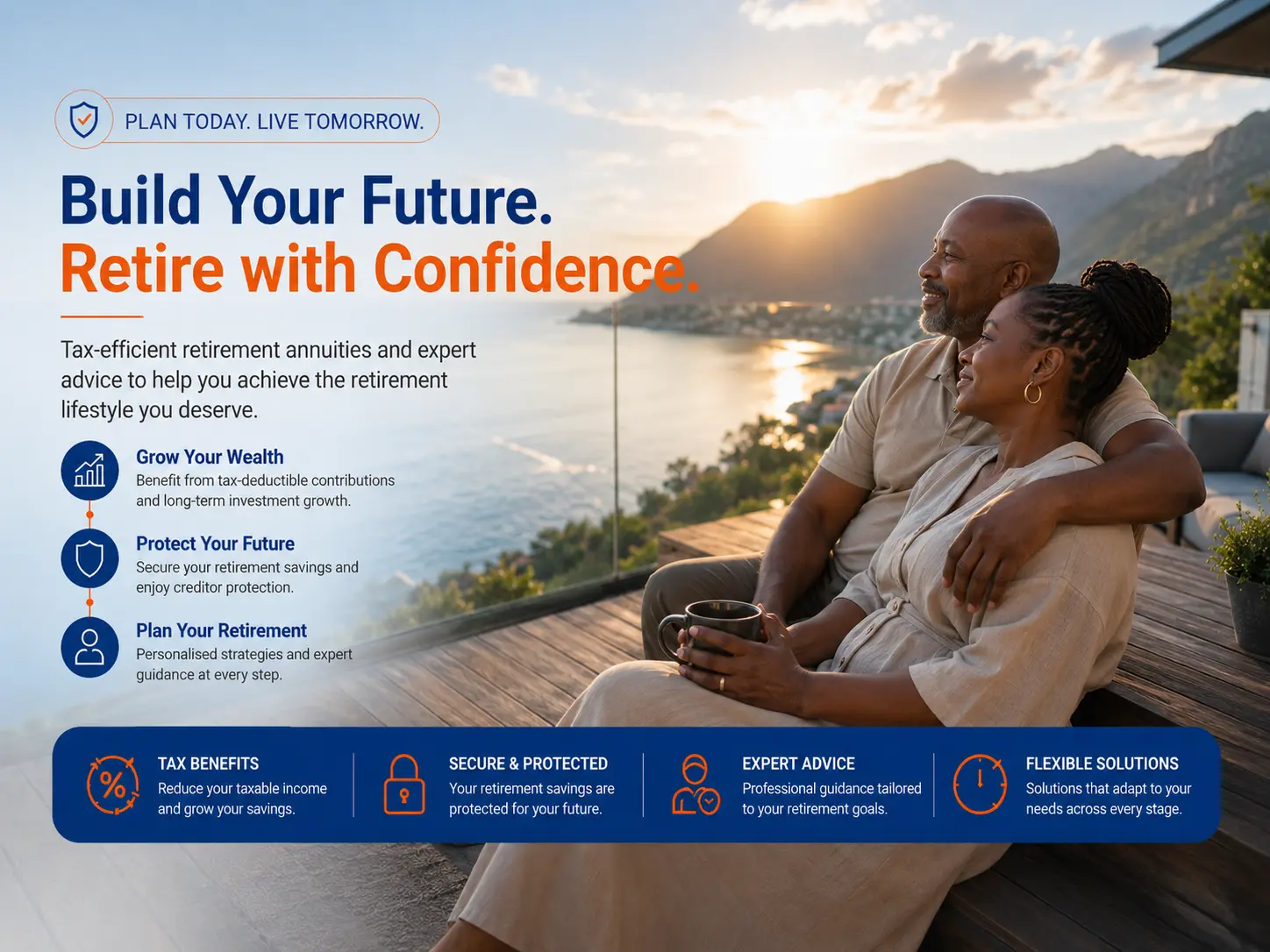

Save for retirement, reduce your tax.

Retirement annuity contributions may qualify for tax deductions within the limits allowed by South African tax legislation — reducing taxable income while building long-term retirement savings. RAs may also offer tax-efficient investment growth during the accumulation phase, helping your capital compound.

We avoid over-contributing without purpose — and help ensure that your retirement strategy remains practical, sustainable, and aligned with your broader financial plan.

- Tax-deductible contributions

Reduce taxable income within SARS limits while saving for retirement.

- Long-term investment growth

Capital compounds over time across diversified investment portfolios.

- Retirement discipline

Funds are preserved for retirement — not eroded by short-term spending.

- Personal ownership

Owned by you — independent of any single employer or job change.

- Creditor protection

May offer protection from creditors in certain circumstances by law.

- Flexible contributions

Monthly debit orders, ad-hoc top-ups, or annual lump sums.

From accumulation to retirement income.

Build, preserve, and convert your retirement capital into a sustainable income — with structured advice at every stage.

Traditional Retirement Annuities

Long-term, tax-efficient retirement savings owned personally — ideal for self-employed individuals, business owners, and employees supplementing employer benefits.

Preservation Funds

Preserve pension or provident fund savings when changing jobs — keep capital invested instead of cashing out.

Living Annuities

Flexible retirement income with continued investment exposure — drawdowns within regulatory limits, with capital still working for you.

Guaranteed Annuities

Predictable income for life or a fixed term — protection against outliving your money and reduced market volatility exposure.

Two-Pot System Guidance

Navigate the savings, retirement and vested components — protect long-term outcomes when access decisions arise.

Retirement Income Planning

Combine living annuities, guaranteed annuities and other capital sources to fund a sustainable retirement income that lasts.

The same goal — very different vehicles.

A pension or provident fund is usually employer-linked. An RA is owned by you — useful where employer cover is missing or insufficient.

Retirement Annuity

- Owned personally — independent of employer

- Suitable for self-employed and supplementary savers

- Tax-deductible contributions within SARS limits

- Flexible monthly, annual or ad-hoc contributions

- Portable across life stages and career changes

Pension / Provident Fund

- Employer-linked — depends on employment

- Often co-contributed by the employer

- Subject to employer scheme rules and choices

- Limited portability when changing jobs

- Often supplemented by an RA for full coverage

Start your retirement plan — digitally, with advice.

Lebon Consulting is an authorised FSP. Submit your information online in approximately five minutes through our secure client portal — our advisers take it from there with a written retirement recommendation.

- 01Submit your information

Approximately 5 minutes through the Lebon Consulting client portal.

- 02We assess your retirement position

Age, income, existing fund balances, tax position and goals.

- 03We model contribution strategy

Across the Sanlam · Old Mutual · Momentum · Discovery panel.

- 04We recommend with advice

A written retirement plan, explained by an authorised adviser.

Five reasons clients trust us with retirement.

Personal ownership of your retirement plan, with professional advice from accumulation through to retirement income.

Personalised retirement planning

Recommendations built around your age, income, affordability, risk profile, retirement age, tax position and desired retirement lifestyle.

Tax-efficient solutions

We help you understand contribution limits, tax deductions and how an RA fits into your broader tax plan.

Long-term investment focus

Disciplined growth over the cycles — not short-term reactions.

Support before & after retirement

Accumulation, preservation and the transition into retirement income.

Professional advice, on the record

Authorised FSP — written recommendations explained clearly.

If any of these sound like you, we should talk.

- Self-employed individuals

- Business owners

- Professionals & freelancers

- Employees supplementing pension

- People between jobs preserving funds

- Clients approaching retirement

- Parents planning long-term security

- Reviewing existing RA contracts

Retirement annuity questions, answered.

The questions clients ask most often before starting or reviewing a retirement annuity. Need something specific? Speak to an adviser.

A retirement annuity (RA) is a long-term retirement savings product that helps individuals save for retirement in a tax-efficient way. It is owned by the individual and is not dependent on an employer.

An RA may be suitable for self-employed individuals, business owners, employees who want additional retirement savings, people without employer retirement benefits, and individuals who want to reduce taxable income while saving for retirement.

Retirement annuity contributions may qualify for tax deductions within the limits allowed by South African tax legislation. A Lebon Consulting advisor can help you understand how this applies to your personal tax situation.

At retirement, your savings are typically used to provide retirement income. This may involve taking a permitted lump sum and using the balance to purchase a living annuity, guaranteed annuity, or another approved retirement income solution.

A retirement annuity is used to save for retirement, while a preservation fund is generally used to preserve retirement savings from a previous employer pension or provident fund when you leave employment.

Retirement annuities are designed for long-term retirement savings and access before retirement is limited by regulation. The Two-Pot system may affect how certain components are treated, depending on the product and applicable rules.

The Two-Pot retirement system is South Africa's retirement reform framework that separates retirement savings into components — including a savings component and a retirement component — designed to allow limited access to part of retirement savings while improving long-term preservation.

Lebon Consulting provides professional retirement planning advice, helping clients understand RA options, tax efficiency, preservation, investment risk and retirement income planning — across a panel of leading providers.

Your retirement starts with today's decision.

Whether you’re starting early, catching up, preserving existing retirement savings, or preparing for retirement income — Lebon Consulting helps you build a structured retirement plan you can rely on.

What you get

- Panel of leading providersSanlam · Old Mutual · Momentum · Discovery

- Tax-efficient structureWithin SARS retirement contribution limits

- Written retirement planOn the record, from an authorised FSP

- ~5 minutes to startSecure online intake