King Price Insurance: Decreasing Car Insurance Premiums Explained for South Africans

How King Price Insurance's decreasing comprehensive car insurance premiums work, what is covered, and how to compare it against other South African insurers.

What this article gets at

Not a brand contest

The right insurer depends on your underwriting, occupation, benefit definitions and long-term affordability.

Escalation matters

The premium you can afford in year one still needs to make sense when the increases compound.

Vitality is behavioural

Rewards can add value, but only when the client actually engages with the programme requirements.

Educational content only. This is not personal financial advice or a guaranteed insurer quotation. Premiums, definitions and outcomes vary by individual underwriting.

On this page

- 01Overview

- 02What is King Price Insurance?

- 03Why is King Price known for decreasing premiums?

- 04How do decreasing comprehensive car insurance premiums actually work?

- 05What does King Price Insurance cover?

- 06What King Price car insurance options should you consider?

- 07Who is King Price Insurance best suited for?

- 08Key features at a glance

- 09What should you check before choosing King Price Insurance?

- 10How does King Price compare with other short-term insurance options on our panel?

- 11What does King Price car insurance cost: premiums, excesses and risk factors?

- 12How do you apply through Lebon Consulting?

Overview

- King Price Insurance is a South African short-term insurer best known for comprehensive car insurance premiums that are designed to decrease monthly as your vehicle depreciates, subject to policy terms.

- The decreasing-premium feature applies specifically to comprehensive car cover, not automatically to all King Price products.

- King Price also offers buildings, home contents, portable possessions and commercial insurance options.

- Premiums and excesses still depend on the vehicle, driver profile, claims history, address, security and underwriting.

- Lebon Consulting is an authorised FSP that compares King Price against other panel insurers to match cover to your needs.

- Always weigh cover limits, exclusions, excesses and claims service, not just the monthly premium.

What is King Price Insurance?

King Price Insurance is a South African short-term insurer that built its reputation on a simple promise: comprehensive car insurance premiums that may decrease each month as the insured vehicle depreciates. For South Africans hunting affordable car insurance without sacrificing comprehensive cover, King Price Insurance is one of the names that comes up early in any comparison conversation.

At Lebon Consulting we advise clients across an 11-insurer panel, and King Price is one of the options we discuss when the brief is comprehensive car insurance with premiums that track the value of the vehicle over time. This article is part of our Insurance Pulse educational stream, and the goal here is clarity, not a sales pitch.

We will explain how King Price works, what cover is available, who the model suits, and what to check before you apply.

Why is King Price known for decreasing premiums?

King Price launched in 2012 with a distinguishing feature: comprehensive car insurance designed to decrease in price each month, in line with the depreciating value of the insured vehicle. Most short-term insurers reduce a vehicle's insured value periodically, but the monthly premium does not always follow.

King Price's pitch is that as your car loses value, the amount the insurer would have to pay out on a write-off drops, so the premium should drop too. That logic resonates with cost-conscious car owners who feel they are paying the same premium for a car that is worth less every year.

The detail to hold in mind: the decreasing-premium feature is specifically tied to King Price comprehensive car insurance, subject to underwriting, vehicle depreciation tables and policy terms. It is not a universal rule across every King Price product.

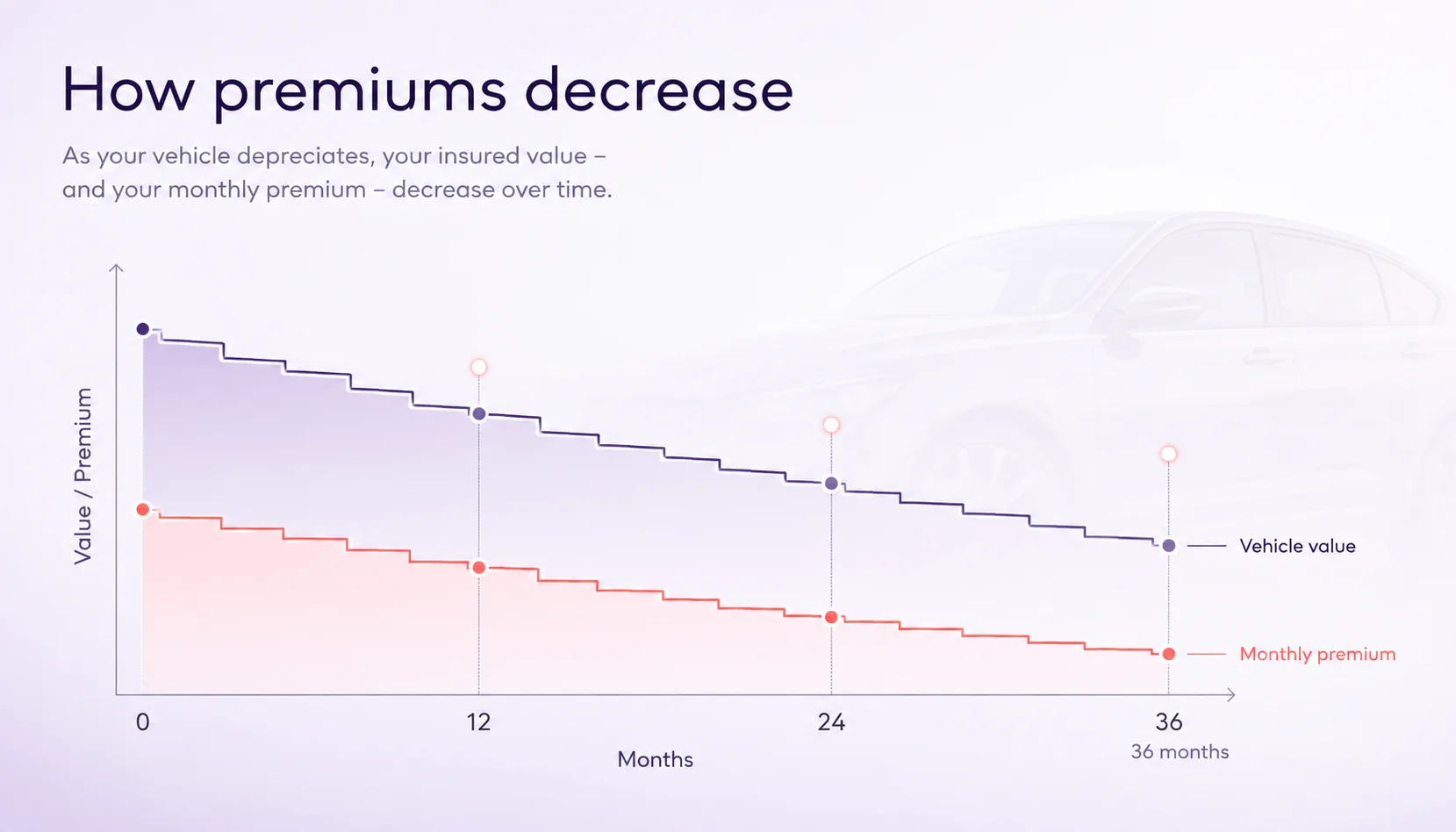

How do decreasing comprehensive car insurance premiums actually work?

The basic mechanic is straightforward. Your car's insured value is recalculated regularly (typically monthly) using depreciation data. As the insured value drops, the premium is adjusted downward in line with the insurer's pricing model.

Several factors influence how steeply your premium decreases:

- Vehicle make, model and age: newer cars and certain models depreciate faster than others.

- Underwriting rules: King Price's actuarial model determines the rate of decrease.

- Claims: a claim can affect future premiums, excesses or rating.

- Annual review factors: risk address, driver profile changes, and updated security can adjust pricing.

The phrase to keep in mind is "may decrease", not "will decrease by a fixed amount". The reduction is designed into the product but not contractually guaranteed at a specific rand value each month.

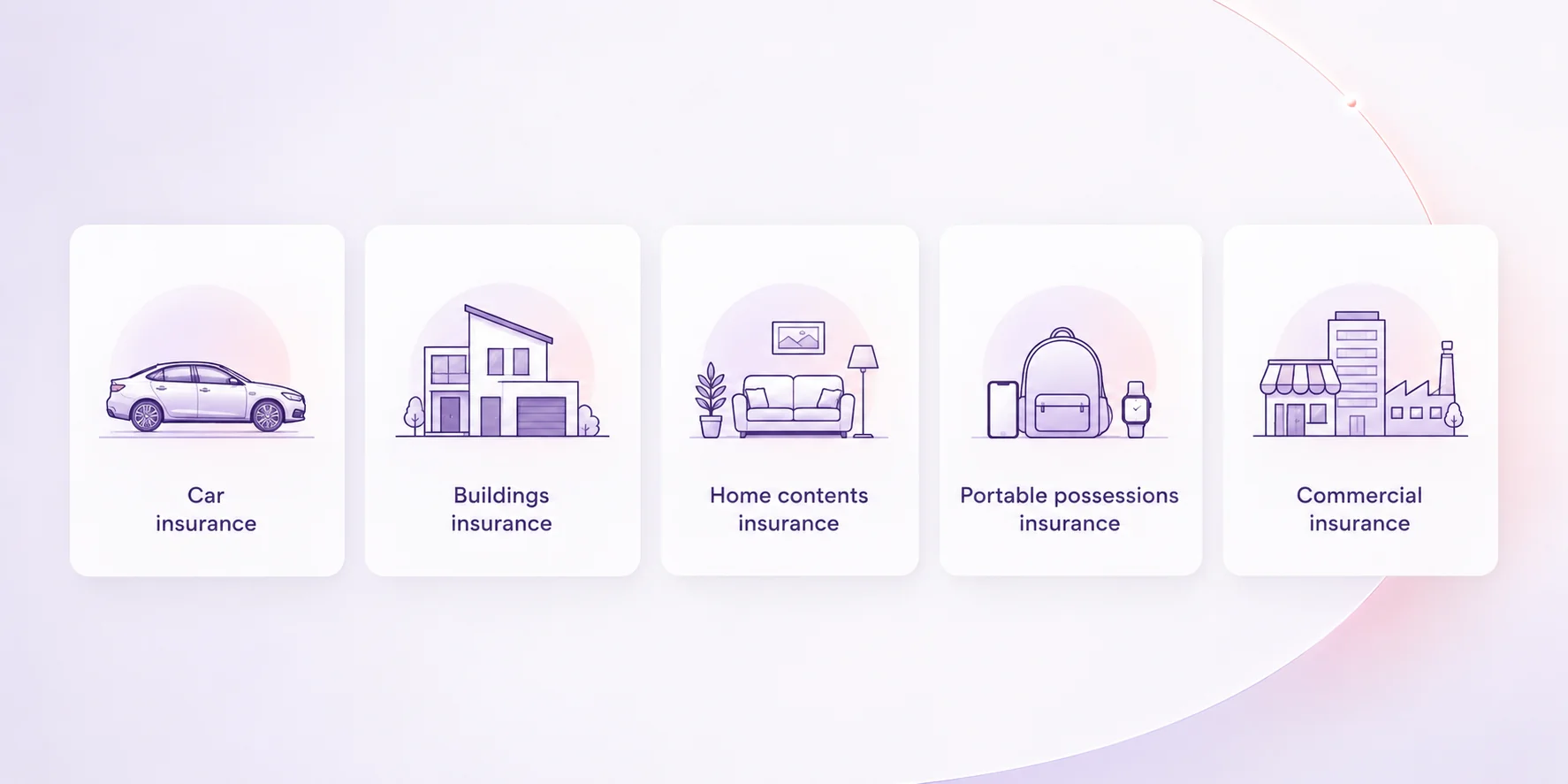

What does King Price Insurance cover?

King Price offers a range of short-term insurance products across personal and commercial lines. The core offerings include:

- King Price comprehensive car insurance: covers accident damage, theft, hijacking, fire and third-party liability, with premiums designed to decrease monthly as the vehicle depreciates, subject to policy terms.

- King Price buildings insurance: cover for damage to the physical structures of a property, subject to policy terms.

- King Price home contents insurance: cover for household contents against insured events, subject to policy terms.

- King Price portable possessions insurance: cover for selected portable items such as phones, laptops and jewellery, subject to policy terms.

- King Price commercial insurance: business, agri, community and engineering insurance options, subject to underwriting and policy terms.

Each product has its own schedule, cover limits and exclusions. The decreasing-premium model is most strongly associated with the comprehensive car insurance product; do not assume it applies in the same way to buildings, contents or commercial lines.

What King Price car insurance options should you consider?

For most South African car owners, the choice typically sits between three cover levels:

- Comprehensive cover: protects against accident damage, theft, hijacking, fire, and third-party liability. This is where King Price's decreasing-premium feature applies.

- Third-party, fire and theft: covers loss caused by fire and theft plus liability to third parties, but not own-damage.

- Third-party only: covers liability to other people's property and vehicles, with no cover for your own car.

If you finance your car, your bank will usually require comprehensive cover. If your car is older and paid off, you may consider scaling down, but for most working car owners a comprehensive policy remains the sensible default.

You can request King Price insurance quotes directly or through an authorised FSP that can compare cover, excesses and premiums across multiple insurers.

Who is King Price Insurance best suited for?

King Price Insurance tends to suit:

- Car owners who want comprehensive cover but are conscious of premium creep over time.

- People who hold onto vehicles for several years and want to feel that the premium reflects the car's falling value.

- Households comparing several short-term insurance South Africa options and prioritising long-run affordability.

- Owners of vehicles that depreciate at a steady, predictable rate.

It may be less ideal for:

- Owners of classic or appreciating vehicles, where a decreasing insured value is not desirable.

- People who place a higher value on specific add-on benefits or claims service features that another insurer prices more competitively.

- Drivers with risk profiles or vehicle types that fall outside the insurer's preferred underwriting bands.

Key features at a glance

| Feature | Detail |

|---|---|

| Comprehensive car premium model | Designed to decrease monthly as vehicle depreciates, subject to policy terms |

| Excess | Standard excess applies per claim, varies by product and risk |

| Personal product range | Car, buildings, home contents, portable possessions |

| Commercial product range | Business, agri, community, engineering |

| Optional add-ons | Subject to underwriting and policy schedule |

| Waiting periods | Where applicable, set out in the policy schedule |

| Claims process | Telephonic and digital, see King Price policy documents |

Premium figures vary widely. Two people insuring the same model can pay very different premiums based on address, driver age, claims history and security. Use our budget calculator to check affordability before committing.

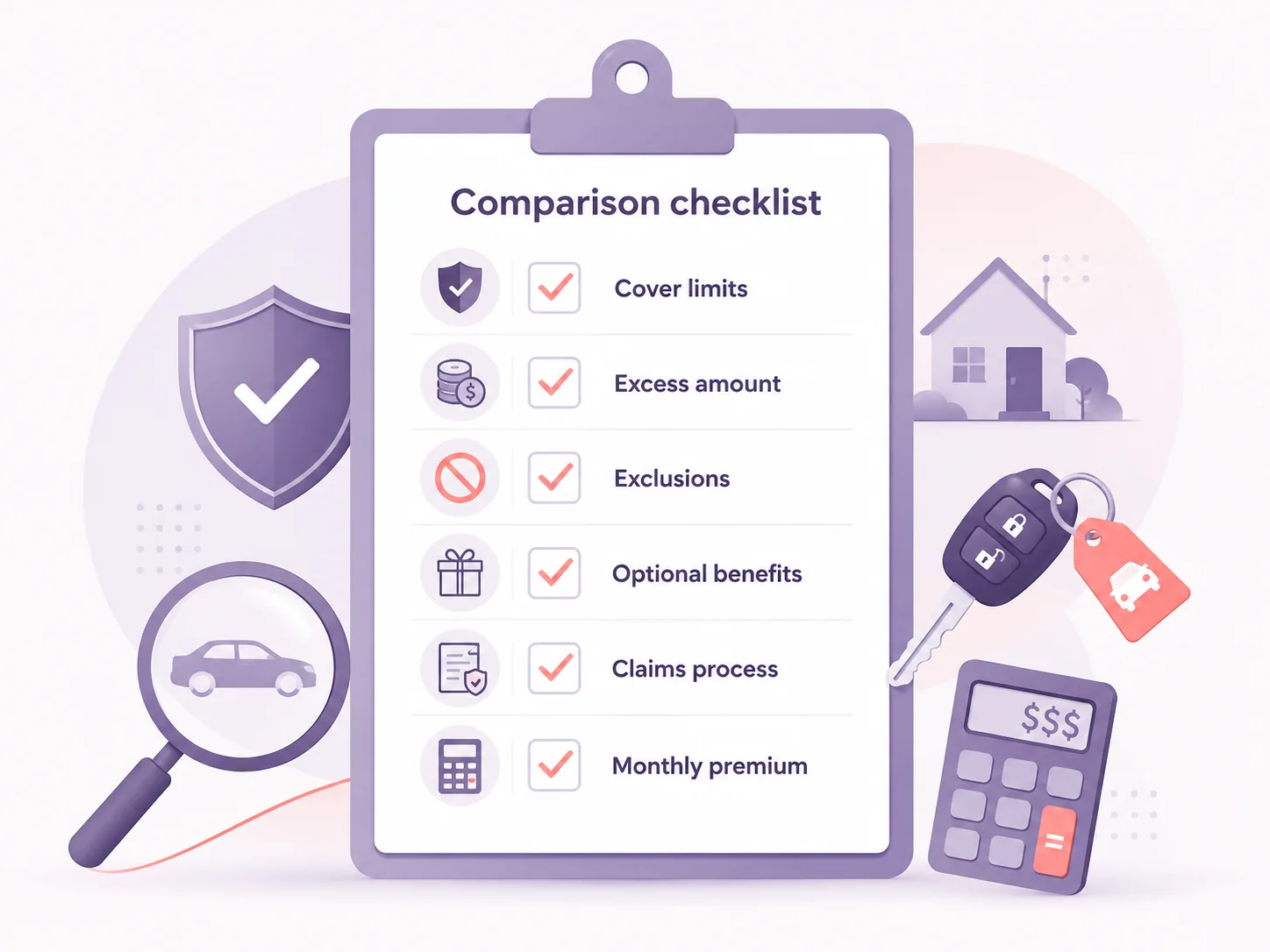

What should you check before choosing King Price Insurance?

Before you commit to any short-term insurance policy, work through this checklist:

- Insured value method: confirm whether the vehicle is insured at retail, market or trade value, and how the value will be recalculated.

- Excess structure: standard excess, voluntary excess, and any additional excesses for young drivers, theft or hijacking.

- Exclusions: read the policy schedule carefully, including driver age restrictions, geographic limits and use of the vehicle.

- Tracking and security requirements: many comprehensive policies require an approved tracking device fitted to the vehicle.

- Claims service: check turnaround times, panel-beater arrangements and rental car provisions.

- Premium escalation rules: confirm exactly how and when premiums decrease, and what could cause them to increase.

A sample broker policy schedule gives a useful sense of the level of detail involved.

How does King Price compare with other short-term insurance options on our panel?

King Price's decreasing-premium feature is distinctive, but it is not the only consideration. Other insurers compete on different strengths: claims service, cover limits, value-added benefits, multi-product discounts, or vehicle-specific pricing.

When we run a short-term insurance comparison for a client, we look across the panel at:

- Total monthly premium over a realistic ownership horizon, not just month one.

- Excess levels and how they interact with the premium.

- Optional benefits like car hire, roadside assistance and credit shortfall cover.

- Underwriting appetite for the specific vehicle and driver profile.

In some cases King Price comes out best. In others, a different insurer prices the same risk more keenly or offers better claims terms. That is exactly why independent advice matters: tied-agent channels can only sell one insurer's product, regardless of fit.

What does King Price car insurance cost: premiums, excesses and risk factors?

There is no single answer to "how much is King Price car insurance". Premiums are individually rated. The key drivers are:

- The vehicle: make, model, year, value, theft statistics.

- The driver: age, licence held, claims history.

- The address: where the car is parked overnight and during the day.

- Use: private, business, or commuter use.

- Security: alarm, immobiliser, tracking device.

- Excess: a higher voluntary excess typically reduces premium.

- Underwriting criteria: insurer-specific rating factors.

A realistic comparison should look at premium, excess, and total cost of risk over 12 months, not just the headline monthly figure.

Remember that short-term insurance protects your assets. It does not protect your income or your family's financial position if you pass away or are disabled. That is the role of life and funeral cover, and for healthcare costs, you should consider medical insurance options alongside your asset cover.

How do you apply through Lebon Consulting?

Lebon Consulting is an authorised Financial Services Provider (FSP No. 52013). We help clients apply for King Price Insurance and compare it against other insurers on our panel.

The process is straightforward:

- We run a needs analysis: vehicle, lifestyle, risk profile, existing cover.

- We request quotes across the relevant panel insurers, including King Price where appropriate.

- We present the options side by side: premium, excess, cover limits, exclusions, add-ons.

- You choose. We handle the application, policy setup and ongoing service.

You can speak to a Lebon Consulting adviser when you are ready to compare options.

This article is for educational purposes only and does not constitute personal financial advice. Product features, premiums and underwriting rules are subject to the insurer's terms and may change. Contact Lebon Consulting (FSP No. 52013) for a personalised recommendation based on your circumstances.

Lebon Consulting

Reviewed by Isaiah Mphaloane, Lead Advisor and Key Individual (FSCA Fit and Proper). Authorised Financial Services Provider, FSP 52013. Articles are reviewed for compliance before publication and reflect the perspective of a licensed adviser, not the product provider.

Continue reading

Frequently asked questions

Does every King Price product have a decreasing premium?

No. The decreasing-premium feature is most strongly associated with King Price comprehensive car insurance. Other products such as buildings, contents or commercial cover are priced on their own terms.

Will my King Price car insurance premium definitely go down every month?

The premium is designed to decrease as the vehicle depreciates, but this is subject to policy terms, underwriting and the insurer's pricing model. It is not a guaranteed fixed reduction.

Can my King Price premium increase?

Yes. Premiums can be affected by claims, changes in risk address, annual reviews and broader underwriting adjustments.

Is King Price cheaper than other car insurance in South Africa?

Sometimes. It depends on the vehicle, driver and risk profile. The only way to know is to compare quotes across multiple insurers.

Do I need a tracking device for King Price comprehensive car insurance?

Many comprehensive policies require an approved tracking device for higher-risk vehicles. Confirm the requirement on your specific quote.

Can I bundle car, home and business cover with King Price?

Yes, King Price offers personal lines (car, buildings, contents, portable possessions) and commercial insurance. Bundling may simplify administration but always check whether bundled pricing actually beats split cover across insurers.

Make Lebon Consulting a Preferred Source

Want South African financial guidance you can trust to show up in Google's AI answers? In Google Search, open Search personalisation → Preferred sources and add lebonconsulting.co.za. Preferred sources are highlighted in AI Overviews and AI Mode.

Recent articles for South African policyholders.

SARS Auto-Assessment 2026: What It Can't See, and When You Should Not Just Click Accept

SARS pre-fills millions of returns from third-party data — but it can't see out-of-pocket medical, donations, side income or RA top-ups. Here's the decision rule before you click accept.

Read article

Tax Calculator 2026 (South Africa): SARS 2026/27 Rates & the Four Levers That Move Your Answer

Calculate your 2026 South African income tax and take-home pay, then watch four legal levers — retirement, donations, a TFSA and your medical credit — redraw where your salary actually goes.

Read article

Anthropic releases Claude Opus 4.8: How to use it to analyse your finances with Lebon Consulting

Lebon Consulting is bringing Anthropic's Claude Opus 4.8 into Lebon AI for bank statement analysis, credit reviews, and insurance gap checks under adviser oversight.

Read articleCompare the panel before you commit to a single insurer.

Request a personalised comparison through the client portal, or speak with an authorised adviser on WhatsApp. We compare across the full Lebon panel — including Discovery, Sanlam, Old Mutual and Momentum.

Next steps

- 01EstimateUse the life cover calculator to frame the need.

- 02CompareReview panel options across premium, benefits and exclusions.

- 03ApplyProceed through the Lebon Consulting client portal when the advice record is clear.

Sources referenced

- https://www.kingprice.co.za/

- https://www.kingprice.co.za/about-us

- https://www.kingprice.co.za/personal-insurance/building-insurance

- https://www.kingprice.co.za/commercial-insurance/business-insurance/about-business-insurance

- https://www.kingprice.co.za/contact-us/helpful-info/view-documents

- https://www.fspsolutions.com/live/Products/KingPrice/Example%20broker%20policy%20schedule.pdf